Introduction

A “Chart of the Century” has been circulating in news media and among health economists, which shows that the price of hospital services has surged over 220% between 2000 and 2022.[1] This increase is greater than that of any other goods and services category, including all medical services, which increased over 130%, and the overall inflation rate of 74.4%.[2] In this report, we investigate whether these price increases are justified by increasing operating costs.

Hospitals often justify their price increases by citing higher expenses due to labor shortages in the health care workforce resulting from the pandemic.[3] However, hospital prices have been rising faster than those for other medical services long before the COVID-19 pandemic’s beginning in 2020. A recent report in Health Affairs Scholar compared hospital service prices to other professional services in the medical sector, including private practice medical doctors, dentists, eye care providers, and other types of providers. The study found that prices for hospital services have been rising faster than those for other professional services in the medical sector every year since 2006.[4]

These prices may be rising faster if hospital costs are also increasing more rapidly compared to other sectors. This report compares the commercial operating costs, net patient revenue from commercial patients, and commercial operating profits of hospitals with different price levels to examine if higher prices are charged to cover higher costs, or instead to generate higher profits.

Methods for Comparing Hospital Prices, Costs, and Profits

National Academy for State Health Policy’s Hospital Cost Tool

The hospital financial data used in this report are from the National Academy for State Health Policy’s (NASHP) Hospital Cost Tool (HCT) dataset.[5] NASHP’s HCT contains hospital financial data on operating profits, expenses, and inpatient and outpatient care for 2022 derived from Medicare hospital cost reports as documented in the Centers for Medicare and Medicaid Services’ (CMS) Healthcare Cost Report Information System (HCRIS).[6] The financial variables we consider include commercial patient hospital operating costs, commercial net patient revenue, and commercial hospital operating profit. All financial variables in our study are presented per adjusted discharge and can be interpreted as a per patient average. Total adjusted discharges are calculated by multiplying the number of inpatient discharges by an outpatient factor, which is the proportion of inpatient to outpatient hospital charges.

Turquoise Health’s Hospital Rate Database

The implementation of the No Surprises Act required hospitals to disclose the negotiated rates that all insurers pay for health services.[7] Hospital price data from 2023 was gathered from Turquoise Health’s Hospital Rate Database.[8] We focus on negotiated prices for the insurer with the greatest market share in each state, as the insurer with the largest market share has the most bargaining power and can negotiate lower prices. Insurer market shares were obtained from the Kaiser Family Foundation (KFF).[9] Using these prices allows us to estimate a lower bound between the relationship of price and profit.[10] Our analysis includes rates paid by insurers in 2022 or 2023 for the 30 most common diagnosis-related groups (DRGs) and the 12 most common Current Procedural Terminology (CPT) codes as determined from external sources.[11]

Aggregate Price Index

Hospitals and insurers negotiate plan-specific prices for each procedure a hospital offers. As a result, there are often thousands of different prices for each hospital in Turquoise Health’s dataset. To simplify the relationship between price and profits, we create an inpatient and outpatient aggregate price index for each hospital. These indices can be interpreted as average prices for each hospital.

Before creating the aggregate price index, we identify a single price for each outpatient procedure or inpatient hospital stay per the CPT or DRG code at every hospital. Next, we weight each CPT or DRG price by how frequently they occur. After the weights and prices for each billing code have been identified, we generate the price indices for outpatient and inpatient procedures. We use the same process to create a Medicare aggregate price index. This allows us to examine not only differences in absolute prices, but also differences in prices relative to Medicare. A detailed explanation of how this aggregate price index was generated is available as an appendix located at the report’s end.

After matching the price data with the hospital financial data, our final sample consists of 1,715 nongovernment, short-term acute care and critical access hospitals in 2022.

Table 1 presents the DRG and CPT codes used in our analysis, along with their corresponding procedures. Full descriptions of each code are available via CMS.[12]

Table 1 — DRG and CPT Codes With Corresponding Procedures

Note: Table 1 describes all diagnosis-related groups (DRG) and Current Procedural Terminology (CPT) codes used in the analysis.

Results

Price Variation Across DRG and CPT Codes

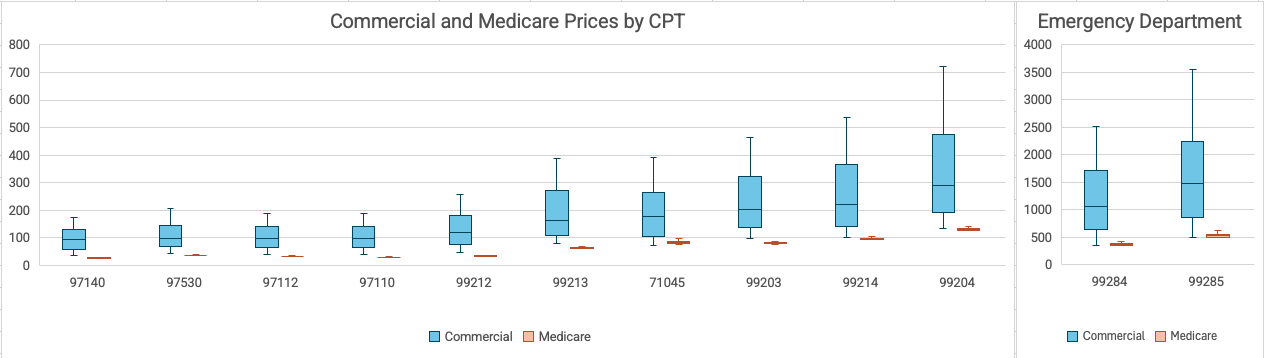

Before analyzing the association between aggregate price and profit, we present the hospital-level price variation for each billing code listed above. Figures 1 and 2 illustrate the variation in prices for CPT and DRG codes, respectively. These figures use box and whisker plots to display the distribution of commercial and Medicare prices for each procedure code. For each code on the horizonal axis, the box above represents the interquartile range of 25th to 75th percentile. The two lines outside this box correspond to the 10th and 90th percentile. The line inside the box represents the median price. Blue plots indicate commercial price distribution, while red plots represent Medicare price distribution.

Figure 1 — Commercial and Medicare Price Variation for Outpatient Procedures by CPT

Note: Figure 1 shows the distribution of outpatient prices in our sample, separated by commercial and Medicare rates. The data is winsorized to the 10th and 90th percentiles, with values outside of this range excluded from the illustration. The outer lines represent the 10th and 90th percentiles, while the upper edges of the box denote the 25th and 75th percentiles, respectively. The line inside of the box indicates the median price. Blue plots represent the commercial price distribution, and red plots represents the Medicare price distribution. CPT codes are shown on the horizontal axis. The left and right panels are separated for scale.

The right side of Figure 1 presents the price variation for 10 of the 12 most common CPT codes. The left panel presents the price variation of expensive emergency department codes, which are separated due to scale differences. Medicare prices vary slightly based on various hospital-level characteristics and are adjusted for population health and other risk factors at the hospital level. The variation in commercial prices for outpatient procedures is substantial. The 90th percentile is between three and seven times larger than the 10th percentile of prices for the same procedure. For example, the 10th percentile price for an emergency department visit with high medical decision making is $486. The price for the same procedure code is $3,549 for hospitals in the 90th percentile. This substantial price variation is found not only on the ends of the distribution but also in the middle of the distribution.

Interquartile ranges (IQRs) measure the variability in the middle of a distribution. They are defined as the difference between the 75th and 25th percentiles. Prices for an emergency department visit with high medical decision making has an IQR of $1,383 and a median price of $1,471. Comparatively, the distribution of Medicare prices for the same emergency department visit has an IQR of $52 and a median price of $529. The very high level of variation is relatively consistent across the 12 outpatient procedures we consider. The least expensive CPT code in our sample is 97140, which corresponds to manual therapy of one or more regions. The commercial price distribution for this procedure has an IQR of $71 and a median of $95. The distribution of Medicare prices for this procedure has an IQR of $2 and a median of $25. The median commercial prices for outpatient procedures in our sample are approximately two to four times higher than median Medicare prices.

For all procedures in our sample, the Medicare prices have very little variation. Recall that these prices are already risk-adjusted for hospital and population characteristics. For outpatient procedures, the lowest commercial prices are often still higher than any Medicare price.

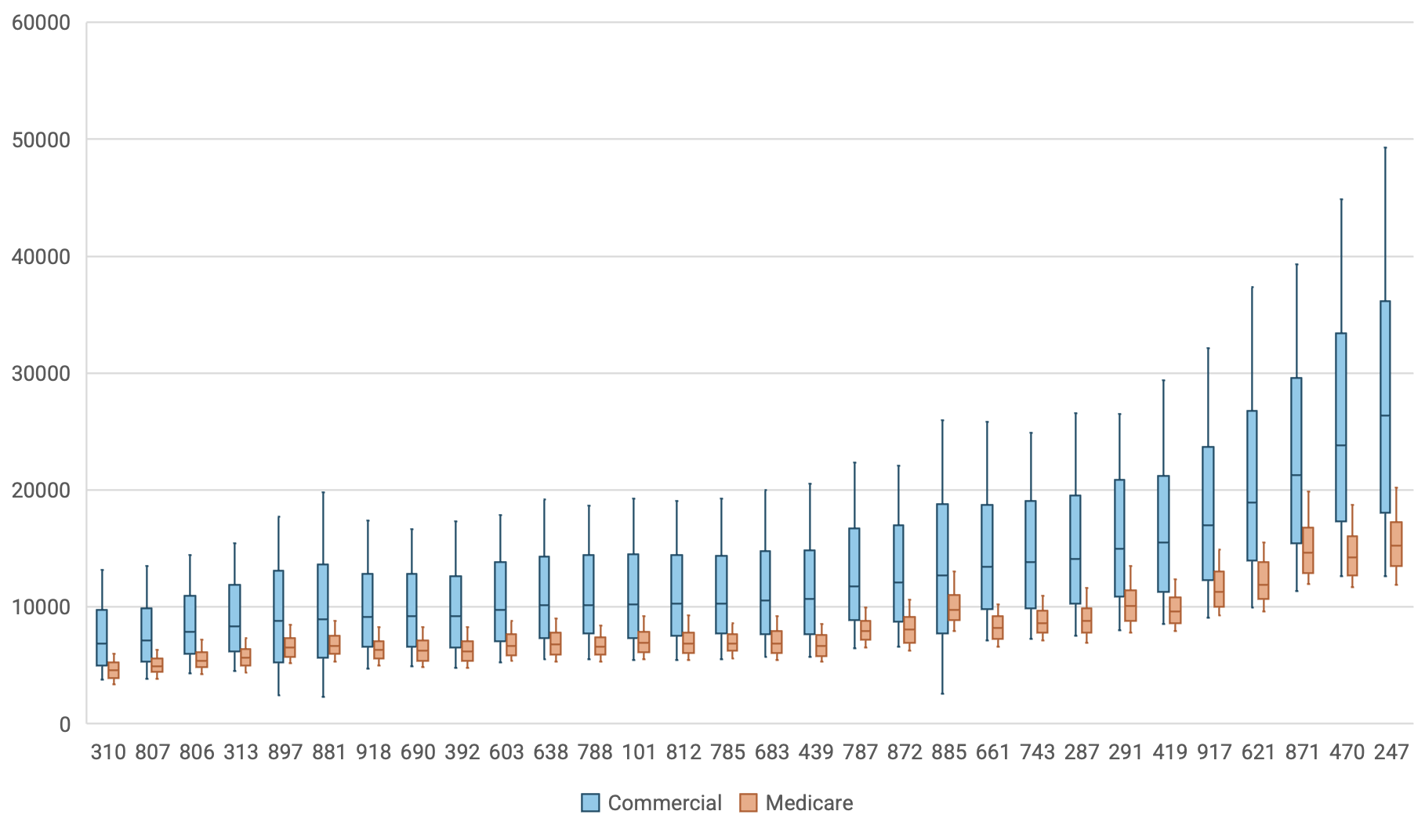

Figure 2 — Commercial and Medicare Price Variation for Inpatient Hospital Stays by DRG

Note: Figure 2 shows the distribution of inpatient prices in our sample, separated by commercial and Medicare rates. The data is winsorized to the 10th and 90th percentiles, with values outside of this range excluded from the illustration. The outer lines represent the 10th and 90th percentiles, while the upper edges of the box denote the 25th and 75th percentiles, respectively. The line inside of the box indicates the median price. Blue plots represent the commercial price distribution, and red plots represents the Medicare price distribution. DRG codes are shown on the horizontal axis. The left and right panels are separated for scale.

Figure 2 presents the price variation for DRG procedures. Again, commercial prices vary significantly more than Medicare rates. Inpatient price variation is similar to what we find among outpatient procedures. The most expensive DRG code is 247, corresponding to percutaneous cardiovascular procedures with drug-eluted stent without major complications or comorbidities. The commercial price distribution for this DRG code has an IQR of $18,083 and a median price of $26,369. The Medicare price distribution has an IQR of $3,703 and a median of $15,233. The variation for all other DRG procedures is similar. The distribution of commercial prices for the least expensive inpatient stay with a DRG code of 310 has an IQR of $4,767 and a median price of $6,889. Medicare prices again had less variation, with an IQR of $1,334 and a median of $4,578. The median commercial prices for inpatient stays are approximately 1.3 to 2 times higher than Medicare prices for the DRG codes in our analysis.

Hospitals’ Aggregate Price, Commercial Operating Costs, and Profits

Next, we examine the relationship between a hospital’s aggregate price and its commercial operating costs, net patient revenue from commercial patients, and commercial operating profits per adjusted discharge using regression analysis. For example, we seek to determine whether hospitals with higher prices also have higher costs, suggesting that high costs reflect a need to charge higher prices in order to cover those costs. To quantify this relationship, we categorize hospitals into quartiles based on their aggregate price relative to other hospitals in the sample. Hospitals may increase commercial prices to offset losses from publicly funded programs. We account for this possibility by including Medicare and Medicaid operating profits or losses and commercial payer mix as additional explanatory variables in our regressions.

Hospitals may also charge higher prices if they provide higher quality care. We include a categorized measure of hospital-wide readmissions to control for the quality of care provided. Lastly, we control for the number of beds at each hospital. We include the price quartile for each hospital as an explanatory variable in regressions where costs, revenue, or profit are the dependent variable, adjusting for the covariates described above. For each specification, we can interpret the coefficients on the categorical price variables as the adjusted difference in profit, costs, or revenue, between each price quartile and the reference group. The reference group contains hospitals in the lowest price quartile.

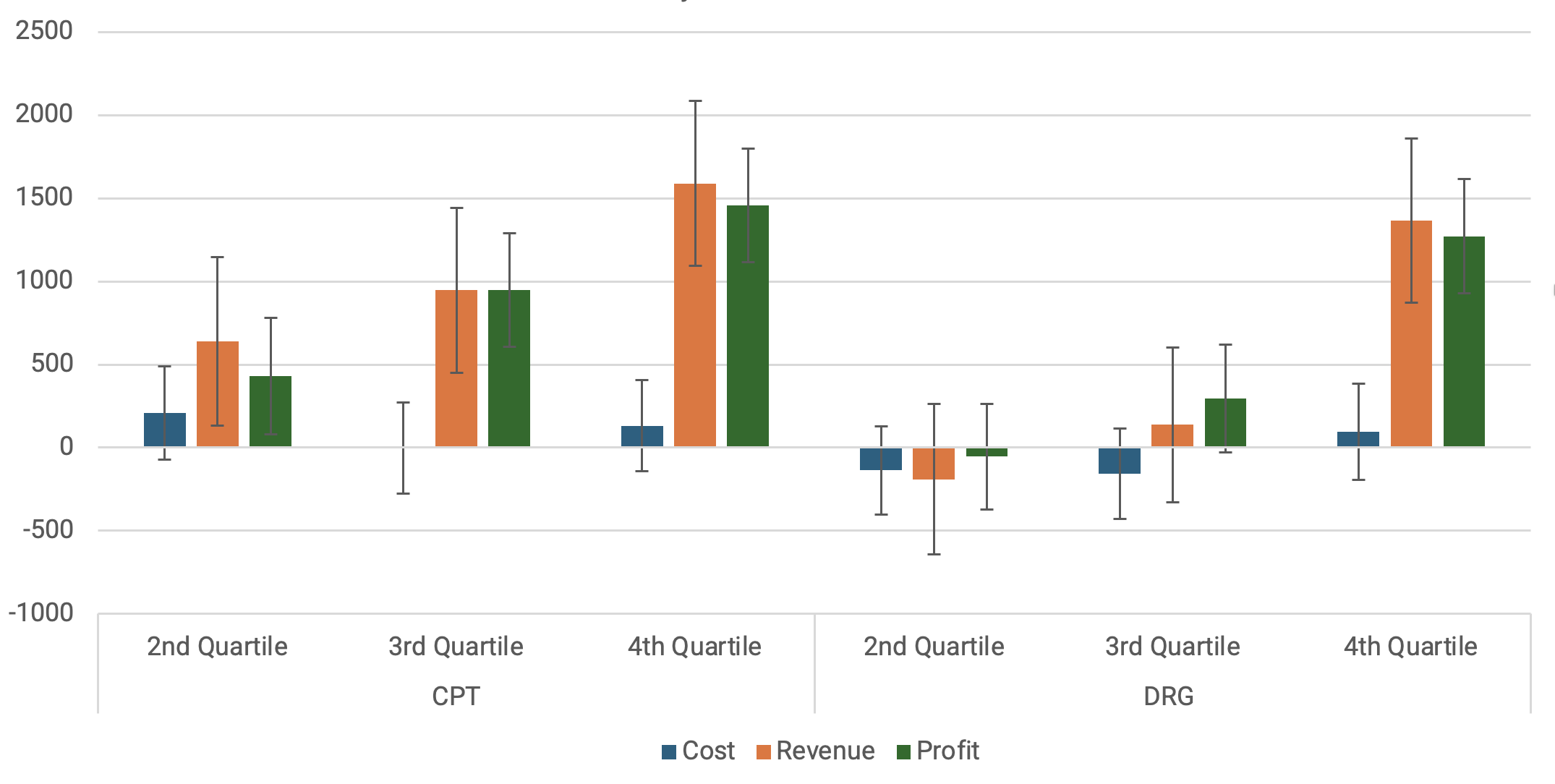

Figure 3 — Differences in Commercial Operating Costs, Revenue, and Profit per Adjusted Discharge Associated With Higher Prices Quartiles, Relative to the Lowest Price Hospitals

Note: Figure 3 presents the estimated average commercial operating costs, commercial net patient revenue, and commercial operating profits per adjusted discharge for hospitals in each price category. These estimates are derived from a regression analysis where each financial variable of interest is regressed on a categorical variable of hospital prices, Medicare and Medicaid operating profits or losses, commercial payer mix, and variables of bed count and hospital-wide readmissions, which are categorized by quartile. The bars in the graph represent the coefficients for each price category variable in the regression. The confidence intervals are shown at the 95% level. The left side of the graph presents the results using the outpatient price index, while the right side uses the inpatient price index.

Figure 3 presents the results from our regression analysis. Each bar corresponds to the adjusted difference in the financial variables considered relative to the reference group. Confidence intervals are presented at the 95% confidence level. The left side of the graph presents the results using the aggregate price index for outpatient procedures. The right side presents the associations of the inpatient price index with costs, revenues, and profits.

Higher inpatient prices are significantly associated with higher profits per adjusted discharges for all price quartiles. Hospitals in the highest inpatient price group earn $1,552 more operating profits per adjusted discharge than hospitals in the lowest price group. This difference is driven by $1,636 more revenue than low-priced hospitals per adjusted discharge. The results are similar for hospitals in the third quartile. We estimate that hospitals in the third price quartile earn $819 more in operating profit per adjusted discharge and $682 more in net patient revenue per adjusted discharge compared to the reference group. Again, there is no statistically significant difference in operating costs. Hospitals in the second price quartile earned $457 more profit per adjusted discharge than the reference group. However, the difference in revenues and costs was not statistically significant.

Altogether, we estimate there is no significant difference in hospital operating costs between the outpatient price quartiles. Higher inpatient prices are associated with higher revenues and profits, but not higher costs.

Next, we analyze aggregate inpatient prices. The right side of Figure 3 presents the adjusted differences in the financial variables considered relative to the reference group, which consists of hospitals in the first price quartile. We estimate hospitals with the highest inpatient prices had higher costs, revenues, and profits compared to the reference group. However, while these hospitals had $671 more in operating costs per adjusted discharge, their revenues were $2,174 higher than low-priced hospitals. These differences allowed high-priced hospitals to average $1,503 more in commercial operating profit per adjusted discharge than low-priced hospitals. We estimate that hospitals in the third DRG price quartile earn $684 more in operating profit per adjusted discharge and $489 more in net patient revenue per adjusted discharge compared to the reference group. However, we do not find a significant difference in costs between hospitals in the third price quartile and those in the lowest price quartile. Hospitals in the second price quartile do not have statistically different costs, revenues, or profits, compared to those in the lowest quartile.

Higher inpatient and outpatient prices are associated with increased revenues and profits, but only higher DRG prices are associated with higher costs. Hospitals that charge higher outpatient prices are not doing so to cover higher operating costs per adjusted discharge.

These associations are similar when categorizing hospitals into four price quartiles using prices relative to Medicare, as well as the absolute prices discussed above. The average price relative to Medicare for all hospitals in our sample is 185% of Medicare prices for inpatient procedures and 325% for outpatient procedures. For reference, this can be compared to the break-even price reported in the NASHP’s HCT dataset, where hospitals in our sample have an average break-even price of 155%. The break-even price represents the price relative to Medicare that hospitals need to charge commercial patients to achieve zero operating profit. Both inpatient and outpatient prices are above this break-even price, with outpatient prices substantially exceeding it.

Figure 4 — Differences in Commercial Operating Costs, Revenue, and Profit per Adjusted Discharge Associated With Higher Prices Quartiles (Relative to Medicare), Relative to the Lowest Price Hospitals

Note: Figure 4 presents the estimated average commercial operating costs, commercial net patient revenue, and commercial operating profits per adjusted discharge for hospitals in each price category. These estimates are derived from a regression analysis where each financial variable of interest is regressed on a categorical variable of hospital prices, Medicare and Medicaid operating profits or losses, commercial payer mix, and variables of bed count and hospital-wide readmissions, which are categorized by quartile. The bars in the graph represent the coefficients for each price category variable in the regression. The confidence intervals are shown at the 95% level. The left side of the graph presents the results using the outpatient price index, while the right side uses the inpatient price index.

Figure 4 presents the results of our regression analysis using price relative to Medicare to create the price quartiles. We estimate similar differences in costs, revenues, and profits between low and high price hospitals when we use relative price as we do with absolute price. Hospitals with the highest outpatient prices relative to Medicare earned, on average, $1,589 more in net patient revenue and $1,457 more in operating profit per adjusted discharge compared to those with the lowest prices relative to Medicare. Similarly, hospitals with the highest inpatient prices relative to Medicare earned, on average, $1,366 more in net patient revenue and $1,271 more in operating profit per adjusted discharge compared to those with the lowest prices relative to Medicare. When using relative prices to define price quartiles, there is no statistically significant association between price quartile and operating costs for either inpatient or outpatient prices.

Conclusion

We find that belonging to the highest inpatient price quartile is associated with 17% higher costs per adjusted discharge and 36% higher commercial revenue per adjusted discharge. These differences result in a 69% higher commercial operating profit per adjusted discharge for the highest priced hospitals compared to those in the lowest price quartile. Similarly, hospitals in the highest price quartile for outpatient prices have 2%, 24%, and 66% higher commercial operating costs, revenue, and profits per adjusted discharge, respectively, compared to hospitals in the lowest price quartile.

Hospitals with higher inpatient prices may have marginally higher costs than lower-price hospitals, they also earn substantially higher commercial revenues per adjusted discharge, leading to higher profits. Hospitals with higher outpatient prices earn significantly higher profits compared to those with lower prices. Meanwhile, higher outpatient prices are not associated with higher operating costs in our sample.

Furthermore, our results suggest that high prices are not simply a response to high operating costs; rather, they are associated with larger hospital operating profits. To promote affordability in the health care system, negotiated rates for health services should remain a priority for policymakers.

Appendix: Creating the Aggregate Price Indices

Inpatient Price Index

Step 1) Identifying the top 30 codes and computing the weights.

First, we identify the top 30 most common Medicare Severity Diagnosis Related Groups (MS-DRGs), as reported by Florida for 2019.[13] Next, we compute the total number of discharges reported for these 30 MS-DRGs and compute what share of total discharges are accounted for by each DRG. These will be used as the weights to create an aggregate inpatient price.

Step 2) Calculating prices.

The raw price data has significant variation in the number of commercial payers across hospitals. It is common for hospitals to have prices listed that represent an obscure out-of-state price that only applies to a handful of cases. Thus, we did not use the median price, because this approach would not account for the frequency with which each price was charged to patients.

We chose to focus on negotiated prices for the insurer with the greatest market share in each start. We assume the largest insurer would have the strongest negotiating power to negotiate lower prices. Using these prices would establish a lower bound on the relationship between hospital prices and profits. Insurer market shares were obtained from Kaiser Family Foundation.[14]

Not all hospitals reported prices for the largest health plan in the state. In these cases, we used the second largest plan; and if that information was not available, we select prices for the third largest plan. We were able to locate prices for one of the three largest payers or insurers in each state for 2,761 hospitals.

Once the prices have been isolated to one health plan for each hospital and MS-DRG, there are still plan specific prices. If there is one Health Maintenance Organization (HMO) price and one preferred provider organization (PPO) price, we calculate the average of these two prices. If there is more than one HMO price, we calculate the median before averaging it with the PPO price. We do the same if there is more than one PPO price.

Even after focusing on the 30 most common DRGs, there are 1,879 cases where hospitals are missing prices for at least one of these diagnoses. To estimate a weighted aggregate price, we need to estimate a price for these missing cases. For this estimate, we use the ratio of the price estimate to the hospitalsMedicare reimbursement rate for non-missing DRGs to derive a proxy for the negotiated price for missing prices.

After estimating a commercial price for each of the DRGs, we use the weights to calculate the aggregate price to generate inpatient prices for each hospital.

Outpatient Price Index

Step 1) Identifying the top 12 procedures and computing the weights.

First, we identify the 12 most common CPT procedures from Definitive Healthcare.[15] Once the procedures are identified, we use the relative frequency of each procedure as the weights.

Step 2) Calculating prices.

Following the same strategy as we used for inpatient prices, we identify a single estimated price for each procedure and each hospital. Again, there are cases where some prices are missing. Just as we do with the inpatient prices, we use the ratio of commercial prices and Medicare prices among non-missing prices and estimate the missing price. Hospitals with more than five missing prices were dropped from the sample.

Once we have prices and weights for each CPT code, we can create and aggregate outpatient prices for each hospital.

Acknowledgement

The authors acknowledge grant support for this work from Arnold Ventures.

Notes

[1] Mark J. Perry, “Chart of the Day … or Century?,” American Enterprise Institute (AEI) (blog), July 23, 2022, https://www.aei.org/carpe-diem/chart-of-the-day-or-century-8/.

[2] Perry.

[3] American Hospital Association, “2023 Costs of Caring,” April 2023, accessed August 5, 2024, https://www.aha.org/guidesreports/2024-05-01-2023-costs-caring.

[4] Salpy Kanimian and Vivian Ho, “Why Does the Cost of Employer-Sponsored Coverage Keep Rising?,” Health Affairs Scholar 2, no. 6 (June 2024): 1–4, https://doi.org/10.1093/haschl/qxae078.

[5] National Academy for State Health Policy (NASHP), “Hospital Cost Tool,” last modified July 2, 2024, accessed August 12, 2024, https://d3g6lgu1zfs2l4.cloudfront.net/.

[6] Centers for Medicare and Medicaid Services (CMS), “Cost Reports,” accessed August 27, 2024, https://www.cms.gov/data-research/statistics-trends-and-reports/cost-reports.

[7] CMS, “No Surprise Act,” last modified April 9, 2024, https://www.cms.gov/nosurprises.

[8] Turquoise Health, “Research Datasets,” last modified July 11, 2024, accessed August 27, 2024, https://turquoise.health/researchers.

[9] Kaiser Family Foundation (KFF), “Market Share and Enrollment of Largest Three Insurers — Individual Market,” accessed August 12, 2024, https://www.kff.org/private-insurance/state-indicator/market-share-and-enrollment-of-largest-three-insurers-individual-market/.

[10] See Anthony T. LoSasso, Kevin Toczydlowski, and Yanchao Yang, “Insurer Market Power and Hospital Prices in the US,” in “Markets, Payments & More,” edited by Alan R. Weil, special issue, Health Affairs 42, no. 5 (May 2023): 615–21, https://doi.org/10.1377/hlthaff.2022.01184.

[11] Definitive Healthcare, “Top 25 Physician Procedures,” accessed August 12, 2024, https://www.definitivehc.com/resources/healthcare-insights/top-25-physician-procedures; FloridaHealthFinder, “Hospital Inpatient Query Results,” Florida Agency for Health Care Administration, accessed August 12, 2024, https://quality.healthfinder.fl.gov/QueryTool/QTResults.

[12] CMS, “List of CPT/HCPCS Codes,” last modified April 18, 2024, accessed August 12, 2024, https://www.cms.gov/medicare/regulations-guidance/physician-self-referral/list-cpt-hcpcs-codes; CMS, “ICD-10-CM/PCS MS-DRG v37.0 Definitions Manual,” accessed August 12, 2024, https://www.cms.gov/icd10m/version37-fullcode-cms/fullcode_cms/P0001.html.

[13] FloridaHealthFinder.

[14] KFF.

[15] Definitive Healthcare.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.