Author(s)

The Big Picture

The most commonly-cited oil demand forecasts — done by the International Energy Agency (IEA), Organization of the Petroleum Exporting Countries (OPEC), and the U.S. Energy Information Administration (EIA) — have seen increasing differences since the COVID-19 pandemic, both in their long-term and, more recently, short-term outlooks. These changes have been accompanied by growing tensions among several major forecasting organizations. In this brief, I track how demand forecasts have diverged, and how the pattern of forecast revisions has also shifted. I argue that a growing focus on the implications for oil demand, in light of more aggressive climate action, is driving these changes by altering organizational priorities. I conclude by discussing how oil market analysts can cope with these diverging forecasts as they become increasingly aspirational.

The Landscape of Energy Outlooks

Something unusual is happening in the world of oil forecasters.

Admittedly, developments in the world of oil forecasters sounds a bit … eccentric. But oil is central in the U.S. and global energy mix — it is by far the largest source of energy used in the U.S. and global economies. As a result, oil price fluctuations remain key for our economic well-being and our politics. Bottom line: This nerd fight matters.

So, what’s going on?

First, a bit of background. In this brief, I will be referring to the main publicly-cited oil outlooks by the IEA, OPEC, and EIA, which is part of the U.S. Department of Energy. Each of these organizations produces a monthly short-term oil outlook, which typically looks ahead a year or two, as well as a separate long-term oil market analysis. While the short-term products for each group are essentially predictions, these organizations’ long-term products, which were most recently published in October 2023, are very different creatures.

- IEA’s “World Energy Outlook” (WEO) provides scenarios of potential future pathways for oil and other energy forms. The current edition includes energy projections through 2050, featuring “Net Zero Emissions by 2050 (NZE) Scenario,” “Announced Pledges Scenario” (APS), and “Stated Policies Scenario” (STEPS).

- OPEC’s “World Oil Outlook” (WOO) provides an outlook for oil and other energy forms — even though the title is focused on oil — as well as alternate scenarios. The current edition includes energy projections through 2045.

- EIA’s “International Energy Outlook” (IEO), which is published every other year, provides a reference case for oil and other energy forms, as well as side cases. The current edition includes energy projections through 2050.

It is not news that these forward-looking assessments disagree — that is entirely understandable, especially given their different structures and analytic differences of opinion. There are no facts about the future! Indeed, I would argue that a healthy disagreement helps decision-makers in industry and government, as these outlooks highlight key areas of uncertainty.

What’s news is that the span of disagreements in recent years have become much larger, and we have seen key players publicly attacking the analysis and motives of other forecasters. From where I sit, I worry that these disagreements seem to stem as much from rhetorical positioning as they do from analytic differences of opinion.

And that’s where the problem lies.

Oil Demand Projections

Growing Disparity in Long-Term Projections

The first divergence to emerge was among the groups’ long-term outlooks on global oil demand.

IEA’s WEO projection for world oil demand in 2030 under STEPS has been revised lower in each of the last three years — even as global demand has increased in each of those years and is now at record levels.[1] The IEA now highlights that demand for oil and other fossil fuels peaks “before 2030” in each of its scenarios, including STEPS. EIA’s IEO has also reduced its 2030 oil demand projection in its latest edition.

While the IEA has consistently reduced the 2030 oil demand projection in its STEPS scenario and the EIA has reduced its demand projection in the most recent IEO, OPEC’s WOO has moved in the opposite direction, generally increasing its projection. The WOO’s 2030 oil demand projection is now 6 million barrels per day (Mb/d) above the IEA’s STEPS projections — and note that STEPS is the IEA’s least aggressive scenario for climate policy and, therefore, its most bullish scenario for oil demand (Table 1).

Table 1 — Global Oil Demand Projections for 2030 by Year of Outlook

Note: Oil demand projections are measured by million barrels per day (Mb/d). These projections exclude biofuels and, where possible, small amounts of gas- and coal-to-liquids.

Large Variances in Short-Term Forecasting

More recently, this discrepancy in oil demand projections has also become apparent in the short-term forecasts, with OPEC’s predictions being consistently more bullish than those by other forecasters.

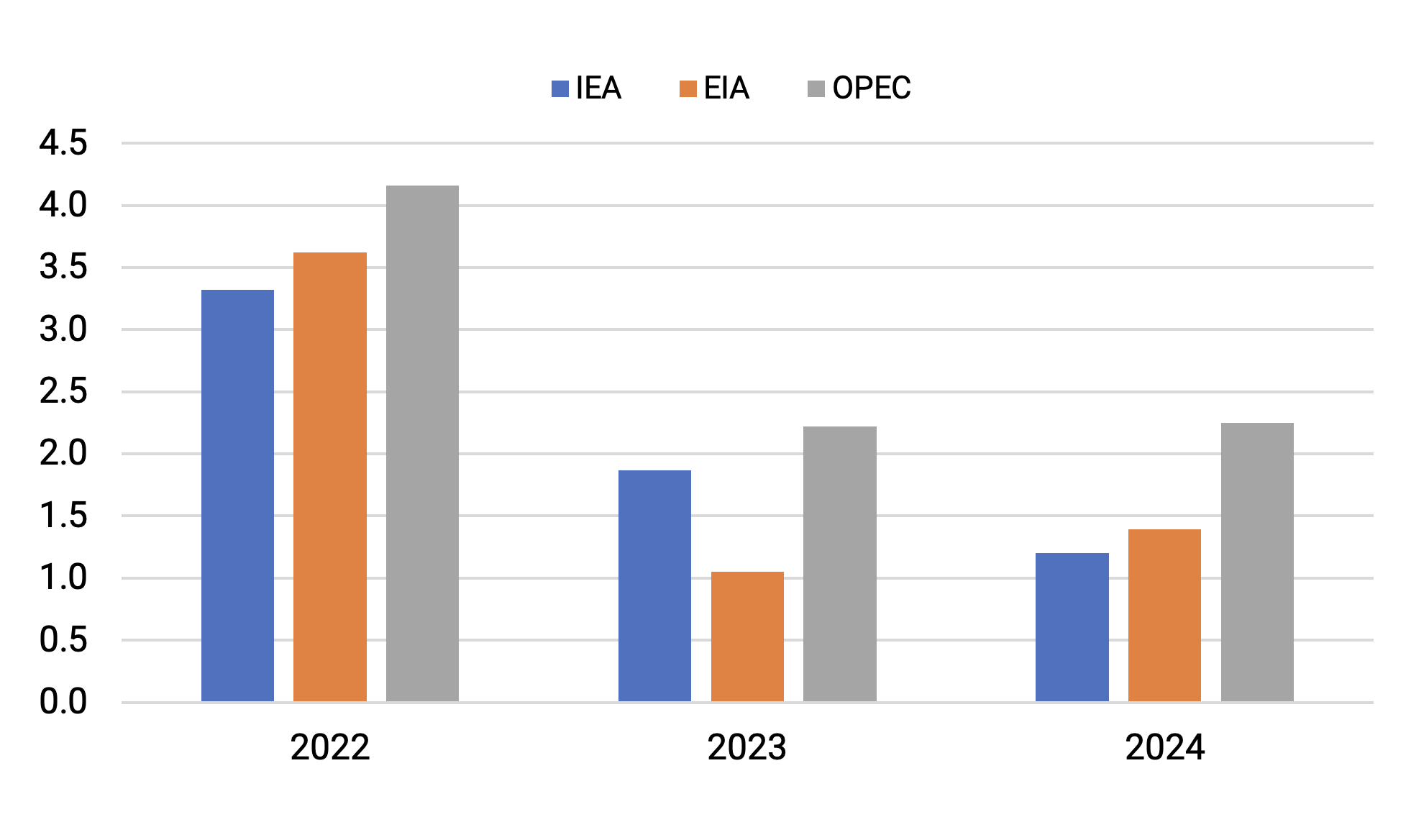

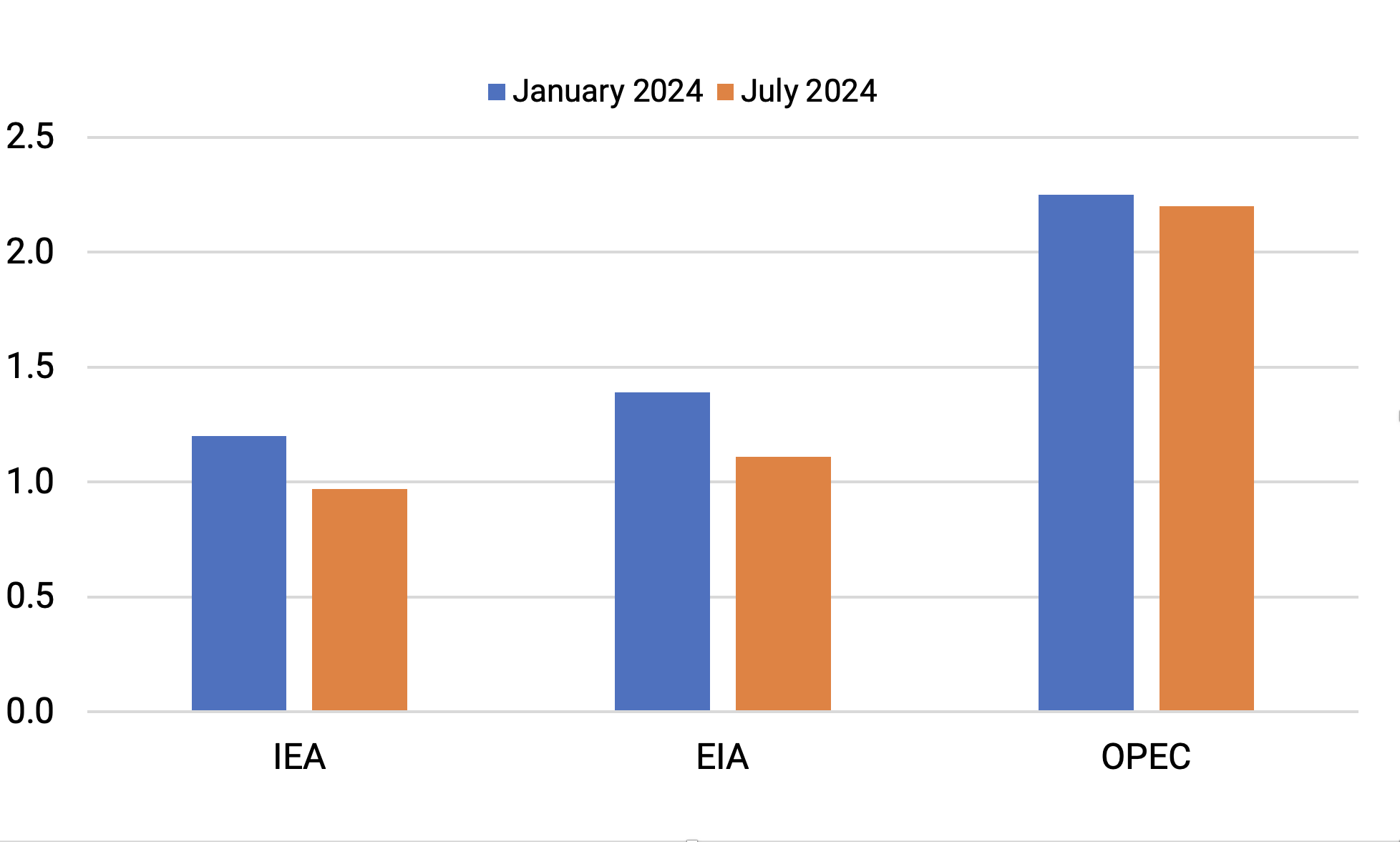

In January of this year, OPEC forecast global demand growth for 2024 of nearly 2.3 Mb/d, significantly higher than either the EIA or IEA, with growth forecasts of 1.4 and 1.2 Mb/d, respectively (Figure 1). That gap has grown since then: In the most recent outlooks, published in July 2024, the EIA and IEA have revised their demand forecasts down to 1.1 and just under 1 million Mb/d, respectively, while OPEC’s forecast has remained essentially unchanged. Moreover, the gap is not merely a function of different opinions on a single country or region but is broadly based.

Figure 1 — Oil Demand Growth Projections in January 2022, 2023, and 2024

Figure 2 — Evolution in Oil Demand Projections From January to July 2024

OPEC’s forecast for growth this year has been an outlier among forecasters. Earlier this year, a demand growth estimate given by Saudi Aramco’s CEO was closer to those of the IEA and EIA.

At this point, the respective forecasters cannot even agree on history. OPEC’s current estimate of 2023 global oil demand growth is 500,000 b/d higher than IEA’s and EIA’s estimates. Similarly, OPEC’s estimate of global oil demand growth in the first half of this year — nearly 2.2 Mb/d — is more than double the estimates of the IEA and EIA at 700,000 and 800,000 b/d, respectively. Typically, historical growth estimates converge over time as better data becomes available. For example, current estimates of 2022 growth between the three groups varied by just a few hundred thousand b/d. Hopefully this will eventually become the case here, but the persistent historical gaps are becoming worrisome.

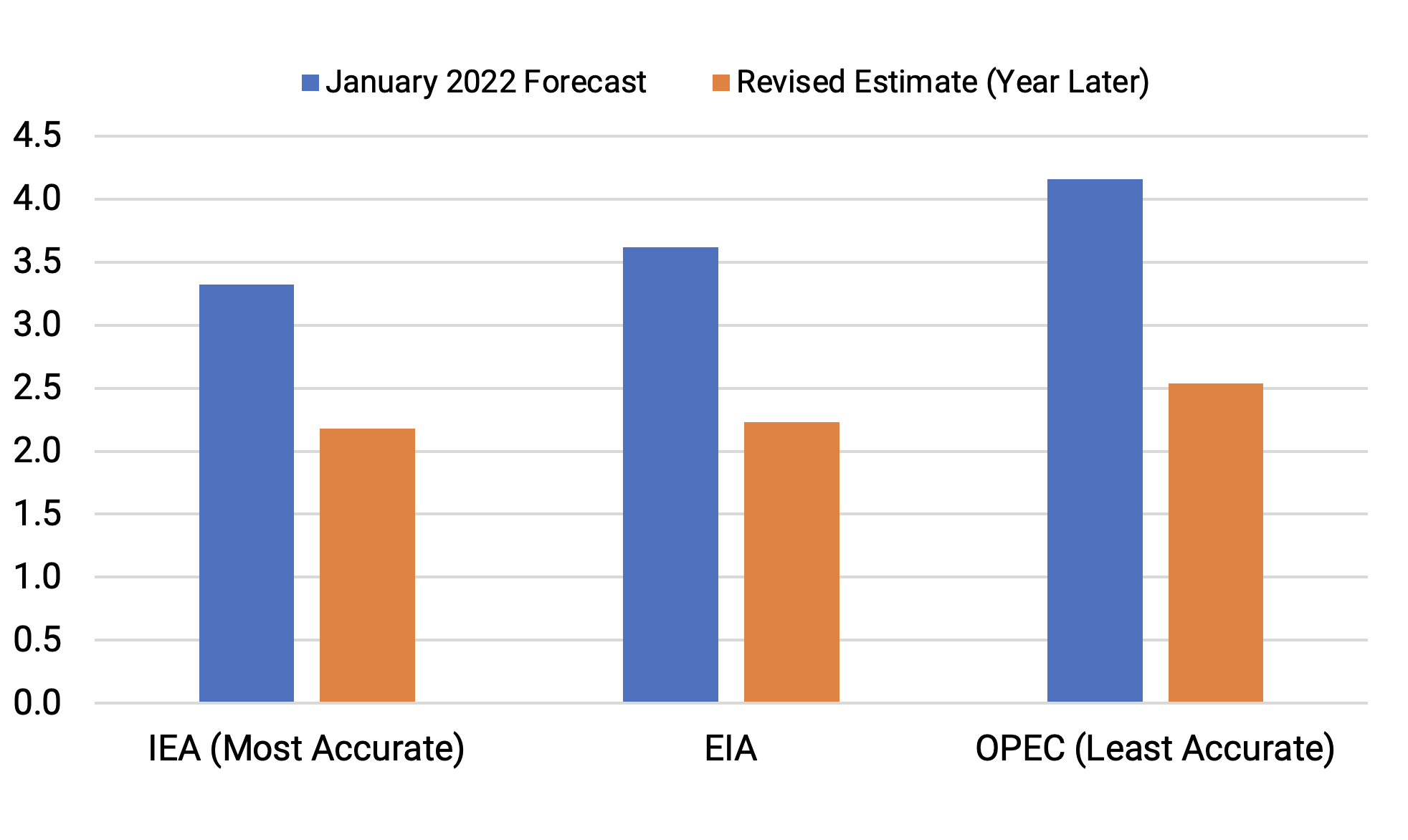

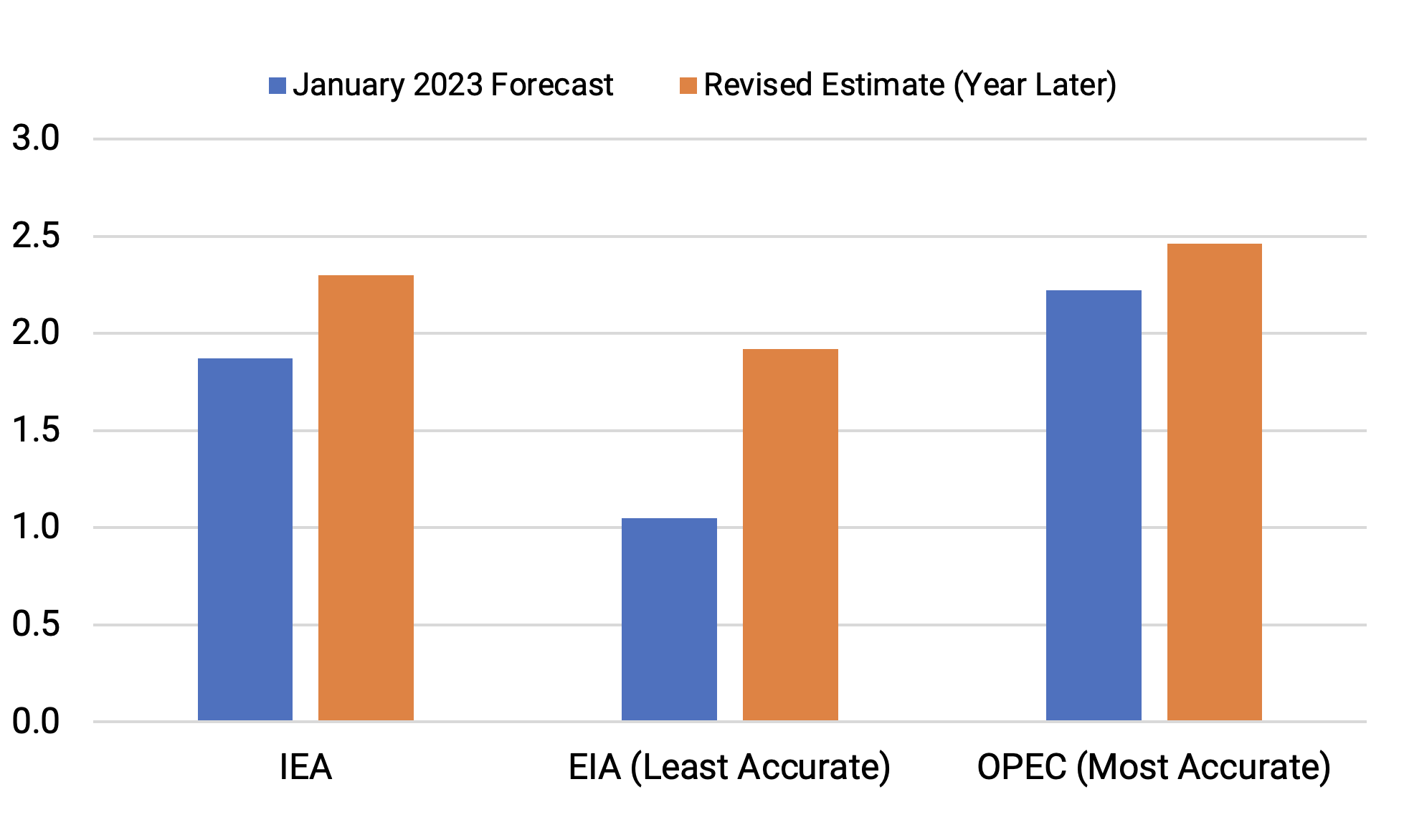

The recent accuracy of the respective forecasters has been mixed. OPEC’s January 2023 forecast was the most bullish of the three and was the most accurate. OPEC’s 2023 outlook for growth of 2.2 Mb/d was higher than the IEA’s at 1.9 Mb/d, and both were well above EIA’s at 1.1 Mb/d). Subsequent revisions show that OPEC was closest to the actual outcome. In contrast, OPEC’s bullish forecast for oil demand growth in 2022 at 4.2 Mb/d) saw the largest error among the three (Figure 3).

Figure 3 — Evolution of 2022 and 2023 Oil Demand Projections

A longer-term historical comparison shows how unusual the current short-term discrepancies are — both for their size and their direction. Going back to 2001, and comparing the forecasts done in January of each year for OPEC and EIA, 2023 and 2024 were by far the largest discrepancies between the two forecaster’s annual demand growth forecasts.[2] As shown in the second panel of Figure 3, in January of 2023, OPEC’s forecast for oil demand growth that year was nearly 1.2 Mb/d larger than EIA’s, and in the January 2024, it was higher by 860,000 b/d. Between 2001–22, the average difference between the two forecaster’s annual oil demand forecasts was only 150,000 b/d.

Moreover, the direction of the difference is unusual: Historically, the EIA has tended to have a higher demand growth forecast — the differences were small, but directionally consistent. OPEC’s January forecast for annual oil demand growth consistently began to exceed EIA’s in 2021, after exceeding EIA’s growth forecast only twice during 2001–20 (in 2009 after the global financial crisis and in 2015).

What’s Changed? Perhaps, Forecasters’ Incentives

Why have these outlooks — both long- and short-term — begun to diverge so widely? Personally, I have always found it useful to consider the institutional biases of an organization when interpreting its analysis.

Note that what follows does not suggest that analytic bias is intentional. For example, EIA is chartered to provide “independent and impartial energy information” within the U.S. Department of Energy. As I will point out, however, organizations — and analysts within them — are shaped by their experience. Analytic biases do not need to be overtly political. In the upcoming discussion, the analytic bias apparent in EIA’s outlooks over the past several decades — discussed in the prior section — may instead reflect the simple, shared reality of how impactful rising oil prices have been for U.S. economic and strategic interests during the past 50 years.

Historically, the institutional calculus was that the U.S. was perceived to be vulnerable to higher oil prices — and as a result, policymakers would complain to the EIA if the oil market was tighter than they had originally forecast. While this analysis does not include IEA’s short-term outlooks, the same institutional pressures can certainly be ascribed to an organization that was created after the oil shocks of the 1970s and whose members are comprised largely of mature, oil-importing countries — as was the EIA. Accordingly, at the margins, the EIA and IEA had an institutional incentive to err on the side of being slightly overly aggressive on forecasting oil demand growth.

In contrast, OPEC forecasters would receive complaints from their members if the market was weaker than they had forecast, since their members are oil exporters and, therefore, vulnerable to lower prices. Accordingly, on the margins, they would have an incentive to err on the side of undershooting on their oil demand forecast. Through 2022 — excluding the COVID-19 pandemic years of 2020–21, when demand fell by a massive, unexpected 10 Mb/d after the January forecasting cycle — the differences in revisions after 12 months reflected that institutional bias:

- OPEC tended to undershoot on its annual demand forecast and would on average revise its oil demand figure up after one year by 130,000 b/d.

- The EIA tended to overshoot on its demand forecast and would on average revise its oil demand figure down by 90,000 b/d.

Interestingly, the pattern of revisions after one year has remained consistent for the EIA even as the U.S. policy narrative has shifted since the country became a net oil exporter, and amid a greater emphasis on climate change: It has continued to tend, on average, to revise lower an overly aggressive short-term demand growth forecast. But for OPEC, the pattern has shifted: Instead of having a low-growth demand forecast that tends to be revised higher, in recent years OPEC has moved to a high-growth forecast that, on average, has tended to be revised lower, largely due to a large overshoot for 2022 oil demand as discussed above.[3]

The historical patterns of relative biases and revisions makes the recent shift even more noteworthy, both in the scale of forecast differences as well as their direction.

Peak Oil Demand Aspirations Shifting Institutional Pressures on Forecasters

A growing focus on risks to future oil demand appears to be shifting perceived institutional biases among oil forecasters, which in turn seems to have contributed to the observed long- and short-term shifts in oil demand forecasts. The concept of “peak oil” is not a new one in oil market analysis. But as public policy increasingly focuses on addressing climate change, especially in the mature economies of the Organization for Economic Co-operation and Development (OECD), analytic attention has understandably begun to focus on those risks.

For many years, the IEA has played a significant role in supporting international negotiations including the U.N. Framework Convention on Climate Change with data and analysis — recently agreeing to expand cooperation “to drive progress on the energy commitments made at the recent COP28 climate summit in Dubai with the goal of limiting global warming to 1.5 °C.” The EIA plays a major role in analyzing the U.S. energy system and energy-related CO2 emissions in support of the country’s commitments under the Paris Agreement, and OPEC has been engaged in the annual U.N. climate change conferences from an early date.

Reflecting the changing priorities of its member countries, in 2021, IEA’s first “Net Zero by 2050” roadmap was published, in which it controversially advised that, under that scenario, “There is no need for investment in new fossil fuel supply.”[4] As discussed above, IEA’s most aggressive scenario for oil demand — STEPS — has continuously been revised lower in recent years.[5] The EIA has constructed side cases in its IEO and in its domestic companion, the “Annual Energy Outlook,” for zero-carbon technology costs, renewables, and many other climate-relevant variables. In 2022 OPEC’s WOO added an “Advanced Technology Scenario, which is aligned with the long-term goals of the Paris Agreement” and has discussed “climate change-related uncertainties” in prior editions.

With these shifting global policy aspirations, the institutional pressures on oil forecasters may reasonably be thought to have shifted as well. The IEA and EIA — organizations situated in countries that have pledged to dramatically reduce fossil energy consumption and CO2 emissions and have called on the rest of the world to do so — face a constant stream of public discussions about their national aspirations. Conversely, political dialogue within OPEC member countries — petroleum exporters — has been more focused on the growth momentum of global oil demand and the defense of benefits that access to oil brings to society.

The Rhetorical Heat Rises

As the forecast differences have gotten larger, key actors have begun to criticize each other’s analysis. OPEC officials have sharply criticized the IEA’s promotion of scenarios that all call for an imminent peak in global oil demand. Notably, Saudi Arabia’s Minister of Energy Prince Abdulaziz bin Salman famously called the new IEA outlook “a sequel to [the] La La Land movie” in mid-2021. While IEA and EIA officials have not directly criticized OPEC’s oil market analysis, relations with producers have suffered in recent years, including a call from the IEA that OPEC should be “very careful” after the group sought to boost oil prices early last year. This, in turn, prompted OPEC to reply that the IEA should be “very careful” about publishing analysis that discourages oil investment.

To be fair, controversy over oil market outlooks goes beyond these three organizations. In the depths of the COVID-19 pandemic, for example, bp argued that global oil demand might never return to pre-pandemic levels, a statement that was quickly criticized by other analysts. While the debate on whether oil demand will peak is widespread, I have focused on these three forecasters because their views are so influential and so widely cited.

What’s an Analyst To Do?

As someone who has watched this space for nearly 40 years, and who prides himself on being a nonpartisan analyst, I worry about the growing disparity among oil outlooks and the heightened tensions among forecasters.

- Where are we to look for objective oil market perspective if the most widely used analyses are increasingly used for advocacy or to score debate points?

- If aspiration is becoming a driving factor for oil outlooks, where do decision-makers go for objective perspective, even if — perhaps especially if — the outlook is seen as unfavorable to those aspirations?

- How can the costs and benefits of alternative courses of action be adequately assessed without an objective starting point?

Admittedly, this may seem like an esoteric topic, but oil market developments and oil policymaking have profound consequences for our economic and strategic well-being —not to mention for sustainability. Rigorous analysis can help us understand how fluctuations in prices at the pump impact inflation, consumer confidence, and our elections and foreign policy.

Of course, forecasts will always disagree. The point of my argument is not for agreement among forecasters. Rather, it is about the growing differences of opinion and the increasing tension among forecasters, and my fear that outlooks are becoming less objective and more aspirational.

Understanding the shifting institutional biases of leading forecasters can help us parse the differences among their outlooks. That does not fix the problem — but it does help the rest of us deal with it, which unfortunately may be the best we can hope for at this point.

Acknowledgements

This brief grew out of a series of private workshops hosted by the Baker Institute Center for Energy Studies on analytic best practices for oil market analysts. Information as of Aug. 1, 2024, was used in preparation of this brief.

Notes

[1] I use the projection year of 2030 because it is the only common reference point cited across the output tables of the IEA, EIA and OPEC long-term outlooks for the years 2020–23.

[2] I exclude the IEA from this historical exercise because its Oil Market Report, including its archive, is only available by subscription. Additionally, short-term comparisons can only be made for oil demand projections, because OPEC — and the IEA — do not forecast OPEC supply and, recently in the case of OPEC, supply from the so-called OPEC+ countries.

[3] In 2023, the recent year in which OPEC’s short-term forecast was the most accurate, oil demand forecasts were uniformly revised higher by the group of forecasters under discussion here.

[4] For the most recent and past editions of the roadmap, see IEA, “Net Zero Roadmap: A Global Pathway to Keep the 1.5 °C Goal in Reach,” September 2023, https://www.iea.org/reports/net-zero-roadmap-a-global-pathway-to-keep-the-15-0c-goal-in-reach.

[5] To be sure, the IEA’s original focus on energy security remains, especially following the Russian invasion of Ukraine and the related spike in energy prices. For a discussion on this topic, see Mark Finley and Anna B. Mikulska, “Energy Transition, Energy Security, and Affordable Fuel: How the Energy Crisis Can Help Policymakers ‘Thread the Needle’” (Houston: Rice University’s Baker Institute for Public Policy, August 5, 2022), https://doi.org/10.25613/2E9H-JX43.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.