The Big Picture

In 1987, the Texas Legislature authorized certain local governmental entities to organize tax increment reinvestment zones (TIRZs). The law allows local governments to create TIRZs that set a baseline value for the property in the zones that is used to determine their property tax receipts for the life of the TIRZs. As property values increase after the zones are created, a percentage, often 100%, of the increase in property tax receipts in subsequent years (referred to as the tax increment) is dedicated to improvements within the zones.

The city of Houston has been very active in creating and expanding TIRZs within its boundaries, forming 28 zones. The first zone, St. George Place, was created in 1990 with the most recent zone, Texas Medical Center, established in 2022.[1] The enabling law allows multiple, overlapping governmental entities to jointly participate in a zone. Other governmental entities currently participate in 17 of Houston’s TIRZs, albeit at substantially lower levels (measured by the percentage of revenues dedicated to the zone) than the city of Houston. The Houston Independent School District (HISD) has been the largest participant but has been scaling back its participation in recent years.

The purpose of the legislation was to provide additional funding to areas with “a substantial number of substandard, slum, deteriorated, or deteriorating structures.” However, this research shows that most of the current tax increment generated and the expenditures made by TIRZs since their inception have been used for improvements in areas of the city with median household incomes almost double the entire city’s median income. This analysis also shows that the amounts of tax increment revenue and total expenditures for TIRZs were positively correlated with higher household median incomes.

TIRZs, Median Incomes, and Tax Revenue

Mapping TIRZs’ Legal Boundaries and Nearby Areas

The area within the TIRZs’ boundaries is quite limited. Only about 85 or 13.3% of Houston’s 640 square miles are included within the TIRZs’ legal boundaries. This is because the boundaries are frequently drawn to only incorporate commercial properties. Nonetheless, the neighborhoods proximate to the TIRZs generally benefit from TIRZ-funded projects.[2] Figure 1 shows the Southwest Houston TIRZ and the nearby census tracks as an example of incongruously drawn boundaries.

Figure 1 — Southwest Houston TIRZ’s Legal Boundaries and Adjacent Areas

Note: The more saturated areas of color demarcate the legal boundaries of Southwest Houston (TIRZ #20), while the lighter areas of color illustrated the selected census tracts for this specific TIRZ. See Appendix B for similar maps of all of Houston’s TIRZs.

To begin to gather and map this data related to TIRZs’ legal boundaries and nearby areas, the following methodology was used:

- Selected census tracts within and surrounding the TIRZs’ legal boundaries as areas that likely benefit from the TIRZs’ projects.

- Initially included all census tracts where any portion of the tract was within 500 feet of a TIRZ boundary, and then adjusting those tracts to eliminate duplicates where a tract was within 500 feet of more than one TIRZ.

- Excluded some tracts if the 500-foot radii included a very small portion of the census tract.

- Made a subjective determination of the areas that would most likely benefit from any TIRZ investment based on natural boundaries, such as freeways, major thoroughfares, and bayous.

- Based this subjective determination on the historic identification of discreet neighborhoods, relying to some extent on Houston’s Super Neighborhood boundaries.[3]

The tracts chosen as those that likely benefit from TIRZ activities comprise about 303 square miles of Houston, which is approximately 45% of the city’s total area. The population of these tracts was 1,249,150 in 2023, which was about 54% of the city’s total population.

Appendix A is a table showing the census tracts assigned to each TIRZ. Appendix B is a collection of maps showing the TIRZ boundaries with the selected census tracts overlaid.[4]

Calculating Median Incomes

To determine the median household incomes, this analysis obtained and reviewed the median household income data from the U.S. Census Bureau’s 2023 American Community Survey. The median income shown for areas that likely benefit from the TIRZs is a weighted average of those median income values for individual census tracts based on the number of households.

Determining Resource Levels of TIRZs

Three metrics to judge the level of resources available to each TIRZ were selected:

- Current Tax Increment Revenue: The tax increment revenue was obtained from the 2023 Annual Certified Financial Report (ACFR) for the 25 TIRZs in this analysis and used the total tax increment revenue as shown in each report.[5] Not all tax increment revenue comes from the city of Houston. Several other entities, primarily HISD, have also participated in some of the TIRZs. According to Houston’s 2023 ACFR, the city contributed $186 million in tax increments, and other participating entities contributed $50 million in fiscal year (FY) 2023.[6]

- Project Expenditures Since Inception: The ACFRs for each TIRZ include a table that shows the amount of project expenditures that are planned by each TIRZ and the amount that has been spent on those projects from the inception of the TIRZ to the date of the report.

- Captured Appraised Value: The Texas State Comptroller’s Office reports total appraised value within each TIRZ as total appraised value, and the amount of that value used to calculate the tax increment each year as captured appraised value. The value of property within the zone during the base year, formally known as the tax increment base value, and of the captured appraised value sums to the total appraised value. This metric shows the amount of the city’s property tax base contained in each TIRZ.

There is, of course, a direct correlation between the current tax increment revenue and the captured appraised value since the latter is used to calculate the former. However, it was important to include the captured appraised value to show the degree to which the city has ceded away its property tax base within the individual TIRZs.

The total expenditures since inception show the cumulative expenditures in each TIRZ. This is the sum of all past amounts of expenditures, and as such, it is a function of how long the TIRZ has been in existence.

Table 1 shows the most recent values of each of these metrics for each TIRZ ranked by median household income.

Table 1 — Summary of Key TIRZ Statistics

Note: A higher resolution version of this table is available here.

TIRZs’ Impacts

Redistributive Effect of Tax Increments

Tax increment zones redistribute property taxes from areas that do not benefit from being included in a zone to those that do. This is because the tax increment revenue reduces the general fund revenue available to the city as a result of fund transfers, and such transfers only finance projects located in the specific TIRZ. Therefore, the incremental property tax revenue does not contribute to other municipal expenses, such as police, fire, health, or general administration, but only to economic or infrastructural improvements within the zone.[7] As a result, the burden of municipal expenses in TIRZs is redistributed to the balance remaining in the city’s general fund, and thus, TIRZs increasingly rely on property taxes paid by taxpayers that reside outside of the areas that benefit from the TIRZs.

Additionally, as TIRZs age, this effect becomes more pronounced as the share of the property taxes captured by the zone increases overtime. In other words, the captured appraised value of a given TIRZ accounts for an increasing portion of the total appraised value as the TIRZ matures. For example, the Midtown Redevelopment Authority, an early TIRZ established in 1994, now collects 90% of the city taxes assessed within its boundaries. As a result, only 10% of the property taxes collected from the Midtown Redevelopment Authority TIRZ go to help defray Houston’s general fund expenses, while the 90% of property taxes taken from and allocated to this zone only funds projects within it.

In FY 2023, the city assessed over $1.5 billion in property taxes. As previously noted, the city rebated $186 million, or about 12% of its property tax assessment, to the TIRZs. The increment revenue rebated to the TIRZs equated to nearly 7% of Houston’s general fund budget. The amount was larger than the budget of all city departments, except for police and fire departments.

The rebate of the tax increment revenue to the TIRZs is the functional equivalent of a subsidy from the city and other participating entities to residents who benefit from the projects within the TIRZs. Since the total population within areas that benefit from the TIRZs is about 54% of Houston’s population, the other 46% of city residents are effectively subsidizing residents that likely benefit from the TIRZs.

Regressive Effect of the Redistribution

The median incomes of the tracts that likely benefit from a TIRZ vary significantly, from $13,850 to $250,001. The average of the median household incomes for the TIRZ tracts was about 17% higher than the city’s overall median income: $73,328 versus $62,637. However, the rebate of the tax increment to the individual TIRZs is highly skewed toward TIRZs with higher household incomes, making the redistribution even more regressive.

There are 11 TIRZs with an average median income that is 50% or more above Houston’s overall median income. The tax increment rebated to those 11 TIRZs in 2023 was $177 million, which, as shown in Table 1, constituted 68% of all TIRZ tax increment rebated by the city. Because of this rebate, the burden of general fund expenses falls more heavily on the census tracts in the city with much lower median incomes.[8]

The population of these 11 TIRZs with higher-than-average median incomes was 419,000. The rebate to the residents of these TIRZs is approximately $422 per person for 2023. As a result, a couple living within one of these 11 areas effectively received an in-kind rebate of nearly $850 from their fellow Houston property taxpayers. The in-kind rebates are in the form of newer and more developed infrastructure — roads, drainage, parks, faster growth in property values, and other development benefits — in nearby areas relative to other non-TIRZ or low increment TIRZ areas.

Thus, across the income distribution, tax increment revenue available to the TIRZs is highly correlated to median household income (Figure 2).

Figure 2 — 2023 Tax Increment Revenue and Average Median Household Income

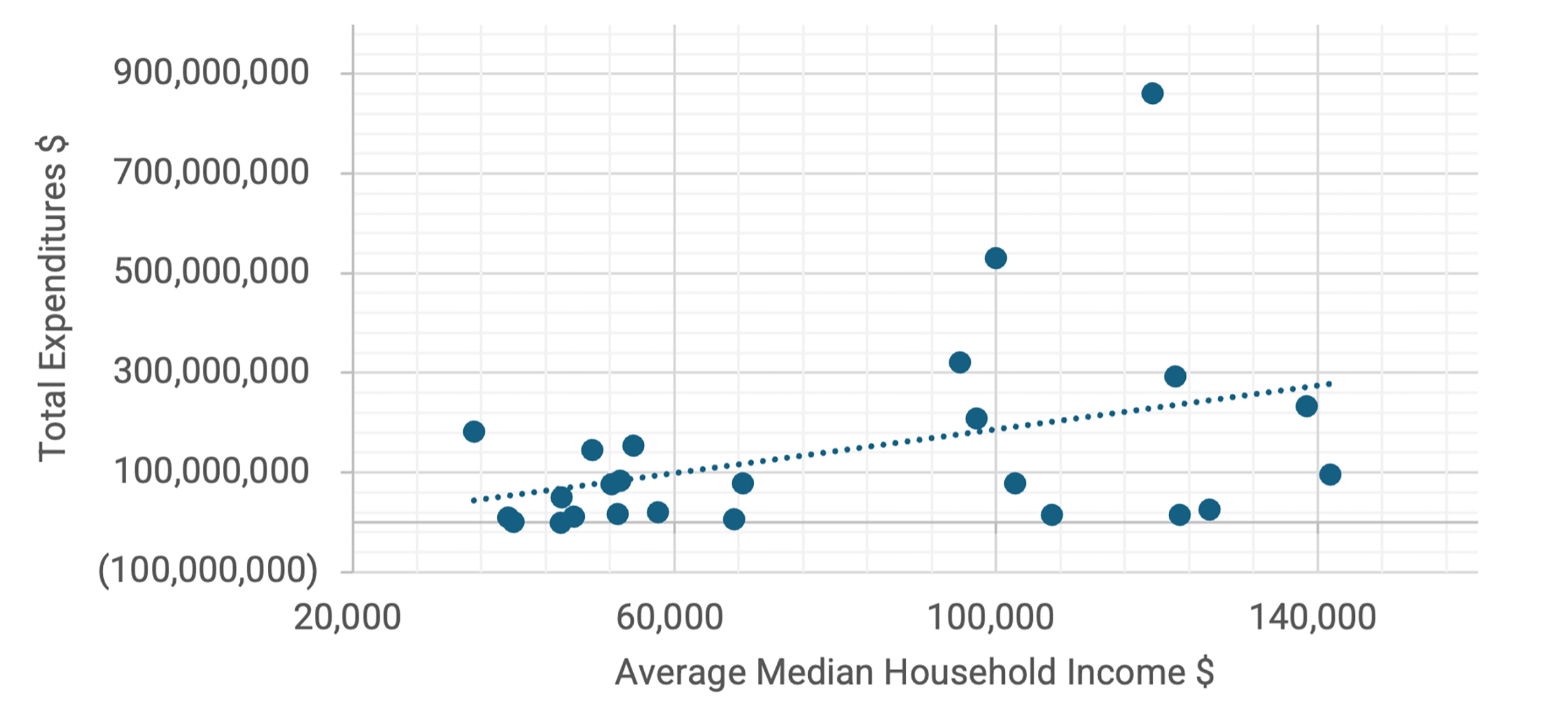

Also, the total amount spent on projects to date is highly correlated to median household income (Figure 3).

Figure 3 — Total Expenditures and Average Median Household Income

Conclusion

It would be a mistake to over generalize about the operations and financial effects of the city of Houston’s TIRZ program. Each of the TIRZs has a unique history, and the manner and scope of their operations vary widely.

However, the claim that Houston’s TIRZs have benefitted affluent areas of the city far more than less affluent areas is clearly supported by the data. While this outcome was clearly not the intent of the Texas Legislature when it allowed local governments to create TIRZs, the anomalous and regressive results of this legislation suggest that substantial reforms are needed to align the outcomes with the original intent of the statute, which was to uplift areas of Houston that needed economic and infrastructural support most.

Acknowledgment

The map analysis and development were supported by Uilvim Ettore Gardin Franco and Bruno Sousa of Rice University’s Spatial Studies Lab.

Notes

[1] For the following reasons, this analysis only includes information on 25 of the 28 TIRZs listed by the city of Houston. The Village Enclaves TIRZ was terminated in 2013. The Texas Medical Center TIRZ has not yet begun operations. The Greater Houston Redevelopment Authority is listed as a TIRZ on the city of Houston’s website; however, pursuant to an interlocal agreement, Harris County funds and administers the TIRZ (“Harris Country Redevelopment Authority and Tax Increment Reinvestment Zone 24,” accessed October 2024, https://harriscountyrda24.org/). It does not appear from this review of the documents and financials that the city has any net contribution in tax increment revenue to this TIRZ. For a listing of Houston’s TIRZs and each TIRZs’ budgetary documents, see City of Houston, “Economic Development: TIRZ Budgets, Agendas, and Documents,” accessed October 2024, https://www.houstontx.gov/ecodev/tirz_info.html.

[2] Some residents in the TIRZs would dispute their neighborhoods have benefited from many of the TIRZ expenditures. Indeed, some of the TIRZ projects have been quite unpopular in the surrounding neighborhoods. However, that is a governance issue regarding how the funds were spent, and regardless of the existence and extent of actual benefits, the resources were available for the benefit of the affected areas.

[3] As the subjective determination could introduce a bias that would skew the results, a separate analysis was prepared to show the results using the 500-foot rule without adjustments. The differences are nominal and do not contradict the basic finding.

[4]There are some census tracts that are near a TIRZ and likely benefit from their projects but are not in the city of Houston. Therefore, those tracts have not been included in this analysis. The city has engaged in “limited purpose” annexations where the city’s legal boundaries are extended to areas for the purpose of imposing sales taxes from that area. However, by agreement with another governmental entity, typically a municipal utility district, the counterparty will provide all typical municipal services and share the sales tax proceeds with the city. The city has also conducted “finger” annexations along major thoroughfares to reach retail establishments and thus impose sales taxes, but the lines are drawn to avoid annexing any residents. None of the special purpose or finger annexations are close to any TIRZ; therefore, those areas have been excluded from this analysis (City of Houston, “Planning & Development: Annexation,” accessed October 2024, https://www.houstontx.gov/planning/Annexation/).

[5] Authors obtained the Annual Certified Financial Reports (ACFRs) for each Houston TIRZ from the city of Houston by request. The city lists “Eastside” as a TIRZ; however, it was never formally created as a TIRZ and, therefore, does not have an ACFR. The city’s ACFR states that it is accounted for as a “special revenue fund.” However, it operates as a TIRZ as a practical matter. For the purposes of this research, the city-approved budget for 2023 was used to obtain the tax increment revenue and total expenditures (City of Houston, “Economic Development — TIRZ: 6. Eastside,” https://www.houstontx.gov/ecodev/tirz/6.html).

[6] This note indicates that the total tax increment revenue for the TIRZs was $236 million. However, the review of the individual ACFRs for the TIRZs showed a total tax increment revenue of $258 million. This analysis has not been able to reconcile this difference, but it may arise from timing differences in the recognition of the transfers between the TIRZs and the city of Houston. Houston’s fiscal year 2023 was from July 1, 2022, to June 30, 2023.

[7] The financial arrangements between the city and TIRZs have grown increasingly complex over the years. The TIRZs pay the city an administrative fee and, in some cases, allowances for affordable housing projects and other municipal services, e.g. additional police overtime. According to the TIRZs’ 2023 budgets, they were scheduled to make approximately $28 million in these payments. However, the same budgets included almost $22 million in grants from the city to support various TIRZ activities. This analysis has not attempted to account for these transfers between the TIRZs and the city due to the lack of data.

[8] For the other 14 TIRZs, their share of shouldering this burden would have been offset by the subsidy they receive. This analysis calculates that the subsidy was about $82 per capita for this group. However, for the TIRZs covering eight of the lowest median household incomes, the subsidy was under $40 per capita.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.